—

In a process costing system, when overhead is applied to production (in this case to the Assembly Department), the journal entry is:

Dr. Work in Process (for the specific department)

Cr. Manufacturing Overhead (applied)

This entry reflects the fact that the company is allocating (applying) manufacturing overhead costs from the overhead pool into the Work in Process account for that department.

Let’s evaluate each choice:

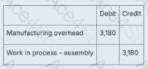

A.

Dr. Manufacturing Overhead

Cr. Work in Process – Assembly

⟶Incorrect: This reverses the correct direction of cost flow. Manufacturing overhead is being incorrectly debited rather than credited.

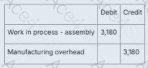

B.

Dr. Work in Process – Assembly

Cr. Manufacturing Overhead

⟶Correct: This entry correctly applies overhead to WIP for the Assembly department.

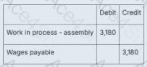

C.

Dr. Work in Process – Assembly

Cr. Wages Payable

⟶Incorrect: This would be the correct entry for applying direct labor, not overhead.

D.

Dr. Work in Process – Wages Payable

Cr. Work in Process – Assembly

⟶Incorrect: This is not a standard entry and incorrectly references "Work in Process – Wages Payable."

Therefore, the only correct entry for applying $3,180 of manufacturing overhead to the assembly department is:

Answer: B

—

[Reference:Saylor Academy – BUS105: Managerial AccountingUnit 4: Process CostingSection 4.2 – How Do We Record the Flow of Materials, Labor, and Overhead Costs?https://learn.saylor.org/mod/book/view.php?id=28818&chapterid=6706, “When overhead is applied to production departments, the company debits the Work in Process account for that department and credits Manufacturing Overhead.”, ]