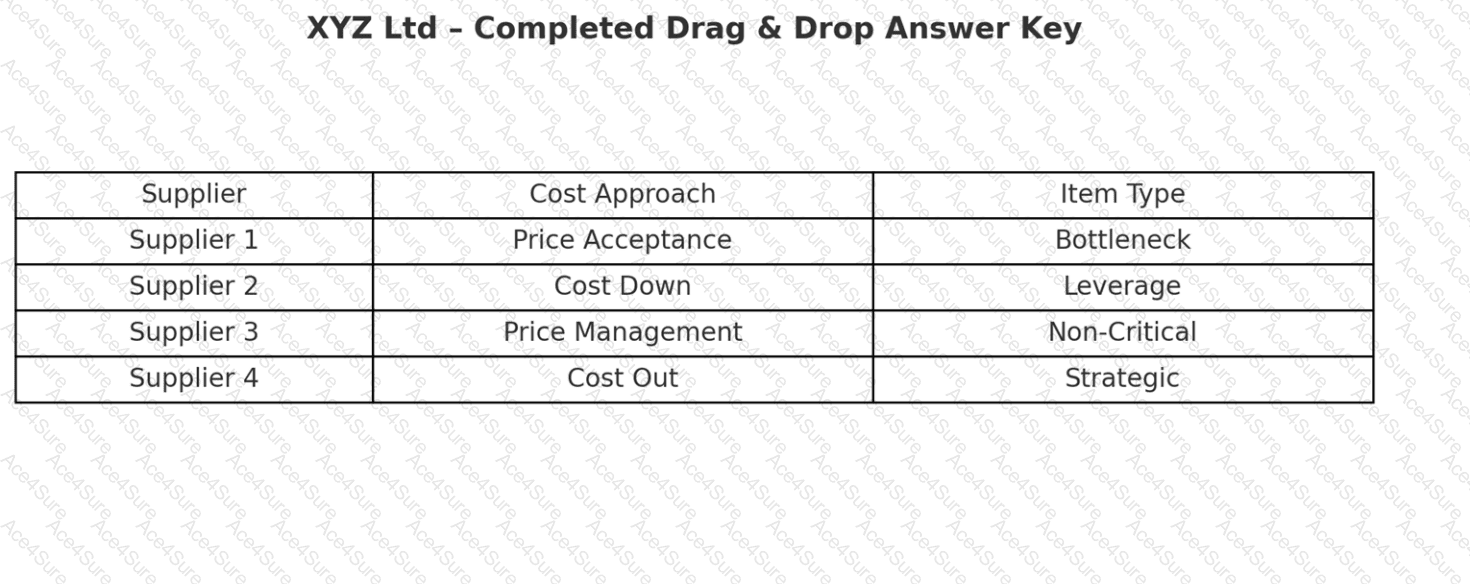

Supplier 1 → Price Acceptance + Bottleneck

Supplier 1 is the sole supplier of a critical item, and XYZ has confirmed through market research that there are no substitutes available. This places Supplier 1 in the Bottleneck quadrant of the Kraljic Matrix, which is defined by high supply risk but low profit impact (or limited ability to influence price). In bottleneck situations, buyers have limited leverage, making them price takers rather than price setters. That’s why the appropriate cost approach here is Price Acceptance—XYZ must accept the price dictated by the supplier because of the absence of alternatives. Procurement’s role becomes risk mitigation, ensuring continuity of supply rather than focusing on negotiation power. The recommended strategies include maintaining strong supplier relationships, holding safety stock, and monitoring supply risks. Price cannot be influenced significantly, so procurement must accept the terms, reflecting a bottleneck scenario.

(Ref: CIPS L5M6 Study Guide, pp.80–83, 97–100 – Cost ApproachesKraljic Matrix)

Supplier 2 → Cost Down + Leverage

Supplier 2 provides items that, while not purchased in large volumes, have a high impact on profit and carry a low supply risk. These characteristics fit into the Leverage quadrant of the Kraljic Matrix: high profit impact, low risk. In such cases, buyers hold strong bargaining power and can use competition or collaborative cost reduction measures to secure better value. The chosen cost approach here is Cost Down, which involves working with suppliers to systematically reduce costs without reducing value. XYZ’s long-term relationship with Supplier 2, combined with a focus on identifying where costs could be lowered, matches the cost-down philosophy. Examples might include value engineering, supplier process improvements, or volume consolidation. Leverage items are ideal for competitive sourcing, e-auctions, and bulk negotiation. By applying a cost-down approach, XYZ can ensure sustained profitability while keeping supply risk under control.

(Ref: CIPS L5M6 Study Guide, pp.80–81, 97–100 – Cost ManagementLeverage items)

Supplier 3 → Price Management + Non-Critical

Supplier 3 provides indirect goods such as stationery, which have little impact on company profits and are purchased regularly in small quantities. These fit into the Non-Critical quadrant of the Kraljic Matrix, which is characterised by low profit impact and low supply risk. In these cases, procurement’s focus should be on administrative efficiency and price management, rather than extensive strategic negotiations. The chosen cost approach here is Price Management, since XYZ meets with the supplier regularly to discuss pricing and bulk discounts. This approach ensures that, although the spend is low-value, the company avoids unnecessary waste or inflated costs. Tools such as catalogues, e-procurement systems, or framework agreements are commonly used in this quadrant to manage spend efficiently. Price management helps free up procurement resources for more strategic categories while still ensuring best value in non-critical areas.

(Ref: CIPS L5M6 Study Guide, pp.80–82, 97 – Non-critical items and price management)

Supplier 4 → Cost Out + Strategic

Supplier 4 is supplying a one-off capital expenditure item. XYZ has engaged in months of negotiations regarding specifications, and both parties are collaborating to reduce costs before manufacturing begins. This aligns perfectly with the Strategic quadrant of the Kraljic Matrix, where items have high profit impact and high supply risk. Strategic items require strong, long-term partnerships and close supplier collaboration. The appropriate cost approach here is Cost Out, which focuses on eliminating unnecessary costs during the design and specification stages, before production. This proactive approach ensures that efficiency and value are embedded in the product from the outset. Cost-out strategies often involve redesign, engineering collaboration, and innovation to reduce total cost of ownership. In such relationships, trust and partnership are critical, since both buyer and supplier must work together to achieve shared value and risk reduction.

(Ref: CIPS L5M6 Study Guide, pp.80, 97–99 – Strategic items and Cost-Out approach)