AAFM CWM_LEVEL_2 Question Answer

Section C (4 Mark)

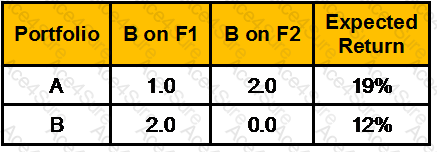

Consider the multifactor APT. There are two independent economic factors, F1 and F2. The risk-free rate of return is 6%. The following information is available about two well-diversified portfolios:

Assuming no arbitrage opportunities exist, the risk premium on the factor F1 portfolio should be __________.

CWM_LEVEL_2 PDF/Engine

- Printable Format

- Value of Money

- 100% Pass Assurance

- Verified Answers

- Researched by Industry Experts

- Based on Real Exams Scenarios

- 100% Real Questions

Get 65% Discount on All Products,

Use Coupon: "ac4s65"