AIWMI CCRA-L2 Question Answer

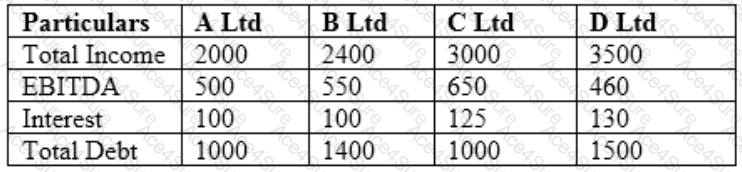

Scott is a credit analyst with one of the credit rating agencies in India. He was looking in Oil and Gas Industry companies and has presented brief financials for following 4 entities:

From the data given below, calculate the standard deviation of the credit portfolio assuming that facility’s exposure is known with certainty, customer defaults and LGDs are independent of one another and LGDs are independent across borrower(s).

Credit Facility A – Loss Equivalent Exposure of $60m, expected Default frequency of 1.5%, loss given default

of 30%, Std Deviation of LGD – 5% and Correlation to portfolio – 0.10

Credit Facility B – Loss Equivalent Exposure of $25m, expected Default frequency of 2%, loss given default of 12%, Std Deviation of LGD – 12% and Correlation to portfolio – 0.45

Credit Facility C – Loss Equivalent Exposure of $15m, expected Default frequency of 5%, loss given default of 85%, Std Deviation of LGD – 18% and Correlation to portfolio – 0.22

- Printable Format

- Value of Money

- 100% Pass Assurance

- Verified Answers

- Researched by Industry Experts

- Based on Real Exams Scenarios

- 100% Real Questions