Saylor BUS105 Question Answer

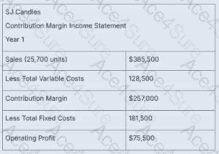

SJ Candles is performing a cost-volume-profit analysis to prepare for year 2. Fixed costs are expected to remain the same as year 1, but variable costs per unit are expected to increase by 10%. They plan to keep the same sales price but want to know what level of sales must be achieved in year 2 to maintain the same operating profit.

BUS105 PDF/Engine

- Printable Format

- Value of Money

- 100% Pass Assurance

- Verified Answers

- Researched by Industry Experts

- Based on Real Exams Scenarios

- 100% Real Questions

Get 65% Discount on All Products,

Use Coupon: "ac4s65"